Illinois pensions remain significantly underfunded, but the trajectory has improved over the last several years due to full statutory payments, supplemental contributions, and strong investment markets.

Earlier this year in February, Gov. Pritzker announced a path to full funding by 2048, building on a 2024 multi-tiered pension plan and recent credit upgrades. The administration plans to accomplish this through three main initiatives:

- Proposing an extension of the state’s pension buyout program to further reduce long-term liabilities and continue to save taxpayer dollars.

- Proposing to direct additional revenues toward paying down Illinois’ pension commitments through transferring unexpected surplus revenues left over after paying income tax refunds.

- Reaffirming commitment to the Governor’s 2024 multi-tiered plan to manage the state’s long-term pension funding commitments, including increasing the statutory funded ratio goal to 100% funded by 2048 and addressing the Tier II safe harbor concerns by adjusting pensionable earnings cap, building on $75 million set aside in the most recent budget.

These individual topics may be covered more in debt in a future blog post, but for the purposes of this one, let’s cover the state of the current system in 2026.

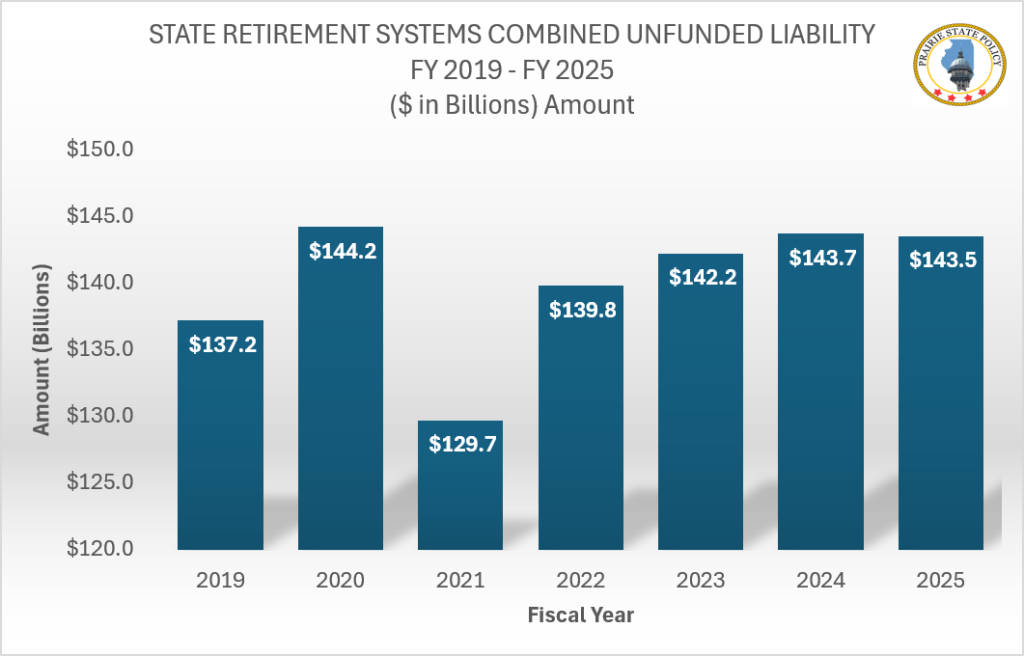

Illinois’ total unfunded pension liability remains at about $144 billion—but has stabilized and modestly improved due to four primary reasons: full statutory payments, additional contributions above the minimum, buyout/acceleration program, and stronger investment returns in recent years due to the recent bull market.

Figure 1 below illustrates the total unfunded liability between all five pension funds.

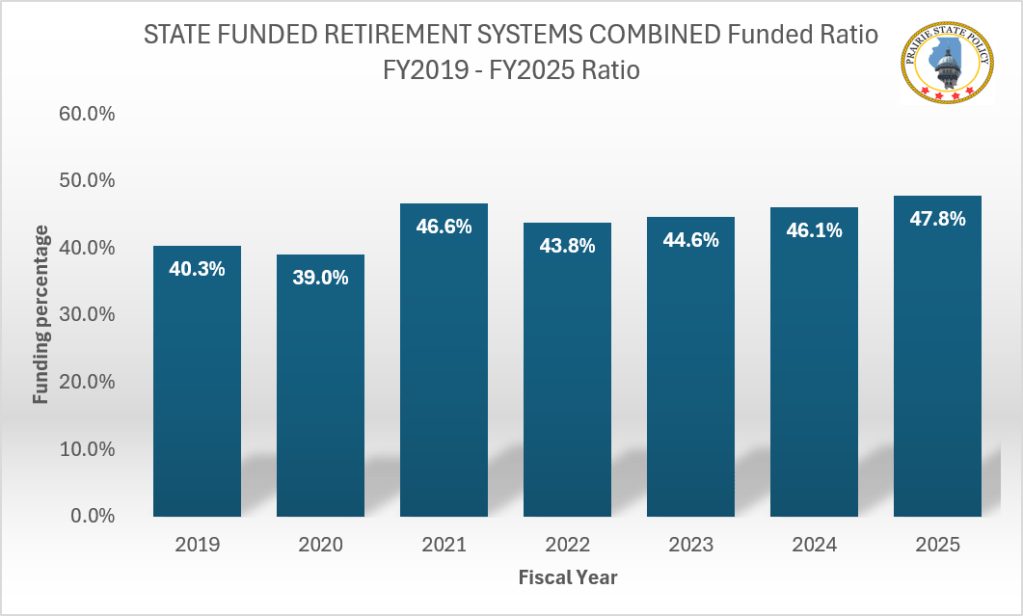

Figure 2 below illustrates the total funding ratio from the five funds combined. Once again, the funding ratio has increased in recent years due to the four primary reasons already mentioned.

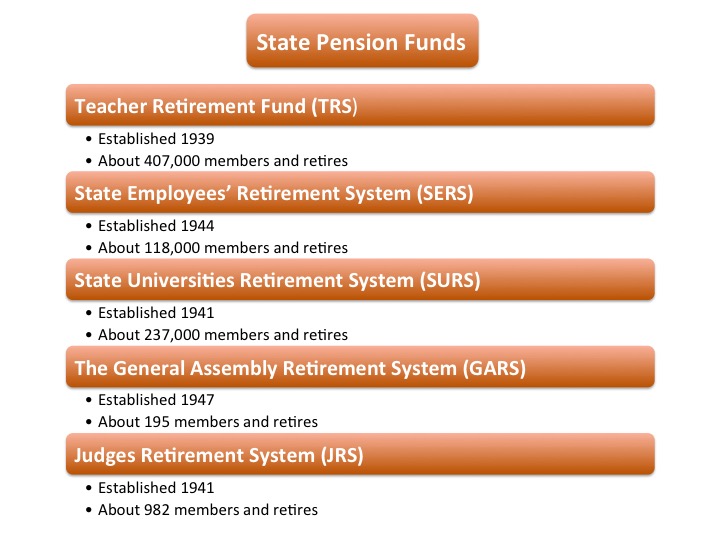

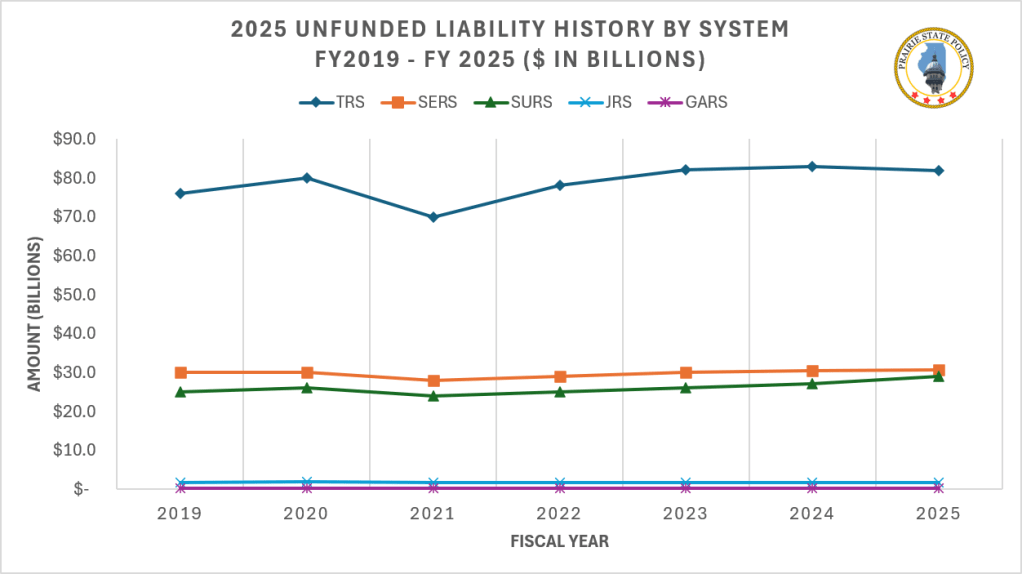

Let’s break this down via the five state systems: TRS, SERS, SURS, JRS, and GARS.

The Teacher’s Retirement System carries the largest unfunded liability because it combines the biggest membership base with the deepest historical underfunding and the most expensive benefit structure. For example, covers all public K–12 teachers outside Chicago, making it the biggest of the five systems. A larger membership base means more accrued benefits more retirees, and more long‑term obligations.

Even if TRS were funded proportionally, its liability would still be the largest simply because it serves the most people. But TRS is not proportionally funded — which magnifies the problem.

What is interesting, however, is that TRS has the highest active‑to‑retiree ratio of the five state pension funds with a ratio of 1.27 : 1. What this means is that for every active worker (participant) in the TRS system, there is one retiree to cover. Unfortunately, this is not the case for the other four funds, as there are more retirees than there are active workers paying into the system.

More pension content to come in the future.

Discover more from Prairie State Policy

Subscribe to get the latest posts sent to your email.