The General Assembly Retirement System (GARS) was established in 1947 to provide lawmakers and certain members of the executive branch with a mechanism to save for retirement. Like Illinois’ other four state‑run pension systems, GARS is structured as a defined benefit plan, offering guaranteed lifetime pensions based on salary and years of service.

Because the Illinois General Assembly has only 177 members at any given time, GARS is by far the smallest of the five systems. Today, the fund has 192 total members, with 132 actively contributing.

GARS faces several structural challenges that stem directly from its size and the nature of legislative service. Membership is optional, and turnover in the General Assembly occurs every two years—especially in the House of Representatives. This creates a persistent demographic imbalance: active contributors can quickly become inactive if they lose reelection or choose not to run again. Their successors may opt not to participate in the system at all.

When this happens, the ratio of active contributors to inactive members shrinks. A smaller active base means fewer contributions flowing into the fund, while benefit obligations remain constant or grow. As that ratio declines, pressure increases on the system’s investment portfolio to generate higher returns to support long‑term benefit payments.

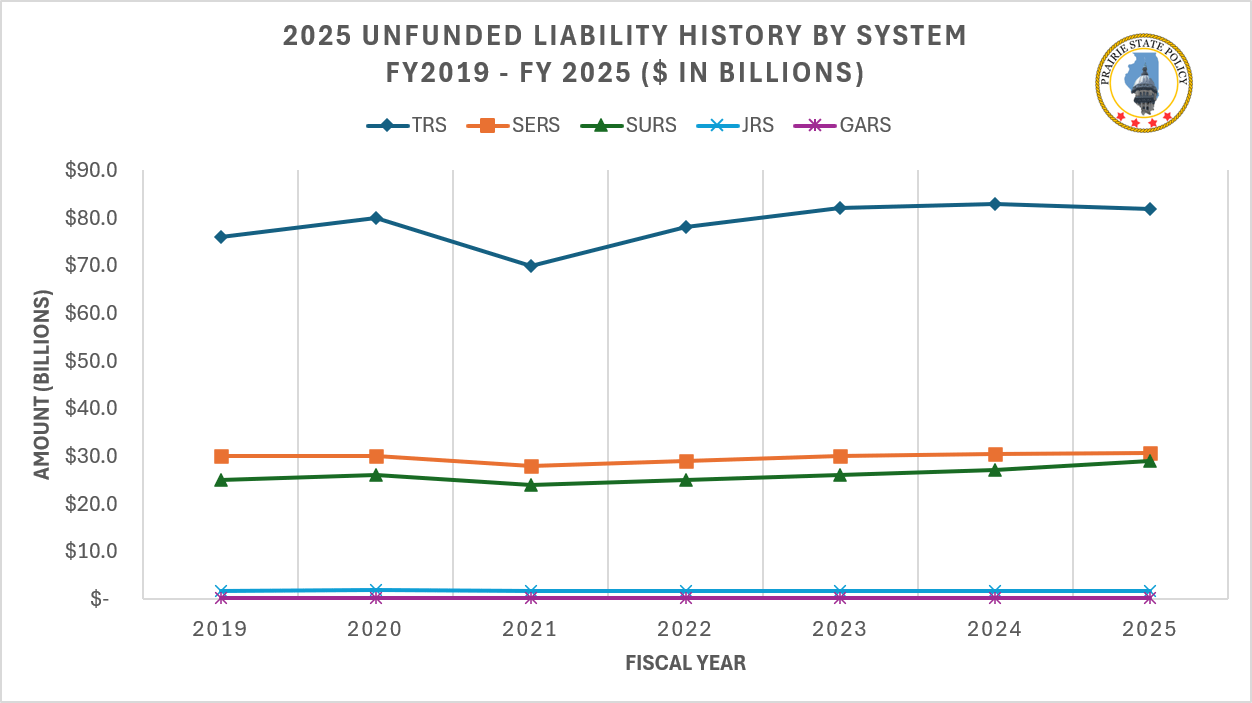

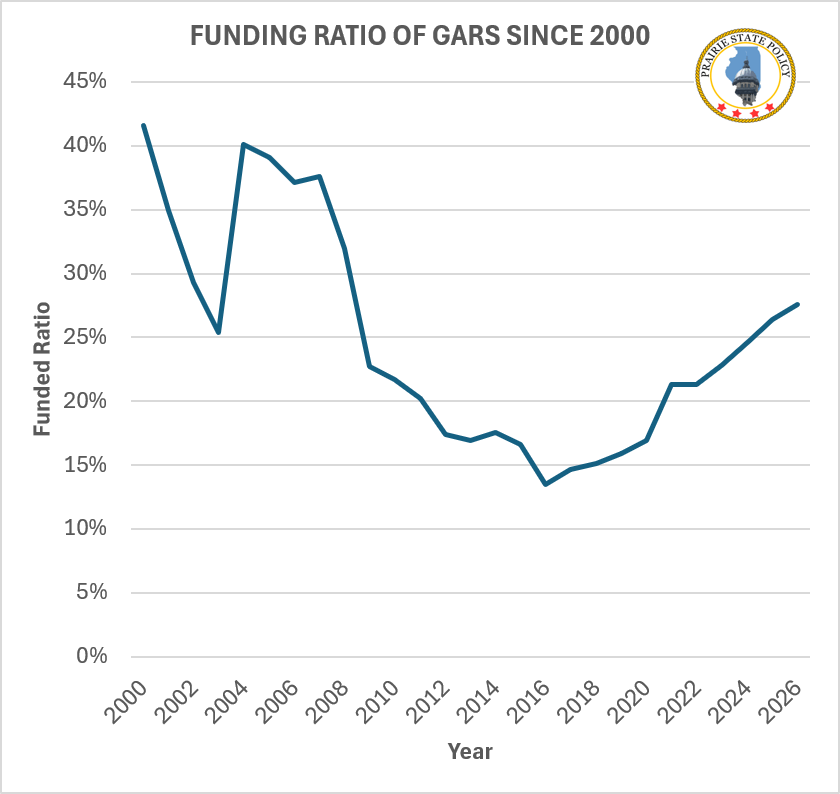

This dynamic helps explain why GARS has the lowest unfunded liability of Illinois’ five main pension funds yet simultaneously has the worst funding ratio, currently at 27.6 percent. Although the funded ratio has averaged roughly 25 percent since 2000, most of the improvement has occurred over the past decade as the system recovered from a difficult period between 2008 and 2016. Figure 1 below illustrates this trend.

Much of the recent recovery is primarily due to (1) improved fiscal management through Tier II reforms and (2) stronger investment performance. The implementation of Tier II in 2010 raised the retirement age and tied the salary cap to the Social Security wage base. As Tier II membership grows, liability growth slows, helping the funded ratio gradually improve.

Illinois also adopted a five‑year smoothing policy in 2017 for changes in actuarial assumptions, ultimately reducing volatility in required contributions and stabilizes the growth of actuarial liabilities.

Because GARS is extremely small, investment performance has an outsized impact on its funded ratio. The FY2025 report shows a 9.9 percent net investment gain, which directly increased the system’s fiduciary net position. Statutory contributions—embedded in state law—have also risen each year, as required payments automatically increase alongside growing liabilities. Together, these factors have significantly strengthened the funded ratio over time.

In short, GARS’ unique membership dynamics—small size, optional participation, and frequent turnover—create ongoing challenges that are far less pronounced in Illinois’ larger pension systems. These structural realities shape the fund’s long‑term financial trajectory and help explain both its historical struggles and its recent, modest improvements.

Discover more from Prairie State Policy

Subscribe to get the latest posts sent to your email.