The following is a continuation of Dissecting Illinois’ Pension Problem Part III: Understanding Tiers

Overview

The State of Illinois’ growing underfunded liabilities was the folly of many and not subjected to a single action. It was the compounded effect of many various decisions made by different individuals over decades. Part IV in our Illinois Pension series documents how the problem started and perpetuated into the issue it is today.

Governor Thompson’s 3 percent annual COLA

In 1989, James Thompson was midway through his second term as governor of Illinois when he signed an amendment to the Illinois Pension Code, which compounded an annual three percent cost of living adjustment (COLA) for recipients of the pension system. The intention was to compensate already retired recipients and downstate and suburban public school teachers, whose pensions where not previously compounded on a yearly basis. In effect, mandating a three percent COLA across the board was a way of compensating underpaid public servants.

According to The Chicago Tribune, The governor’s press release on the legislation highlighted a teacher earning a pension of $16,260 a year as a public servant would benefit from the annual three percent compounded COLA. The legislation was quickly passed through the House and Senate without much analysis. However, the expectations backfired and the COLA is one of the main culprits enhancing the systems liabilities and impeding reform.

In the private sector, pensions are paid out to recipients based on the revenue gained from contributions from payroll, what they’ve received through investment earnings, and, if applicable, Social Security benefits. Social Security’s COLA benefits fluctuate with the rate of inflation. In effect, in years that yield low or negative inflation, like 2009, 2010, and 2015, Social Security recipients do not receive annual increases to their benefits. Consequently, Illinois’ recipients receive their three percent COLA every year, regardless of the rate of inflation or the desperate financial state of Illinois’ pension systems. This has caused the system to become fiscally unsustainable.

The three percent annual COLA acts as a defined benefit system, meaning that pension recipients are rightfully due the benefits promised to them. Because the COLA does not fluctuate with the rate of inflation, unlike social security, recipients are still due what was promised to them even though benefits may not suffice with current economic conditions. The amount paid to recipients is vested with future economic forecasts, and if those assumptions and wrong, the result is a shortfall in the pension system.

The Edgar Ramp

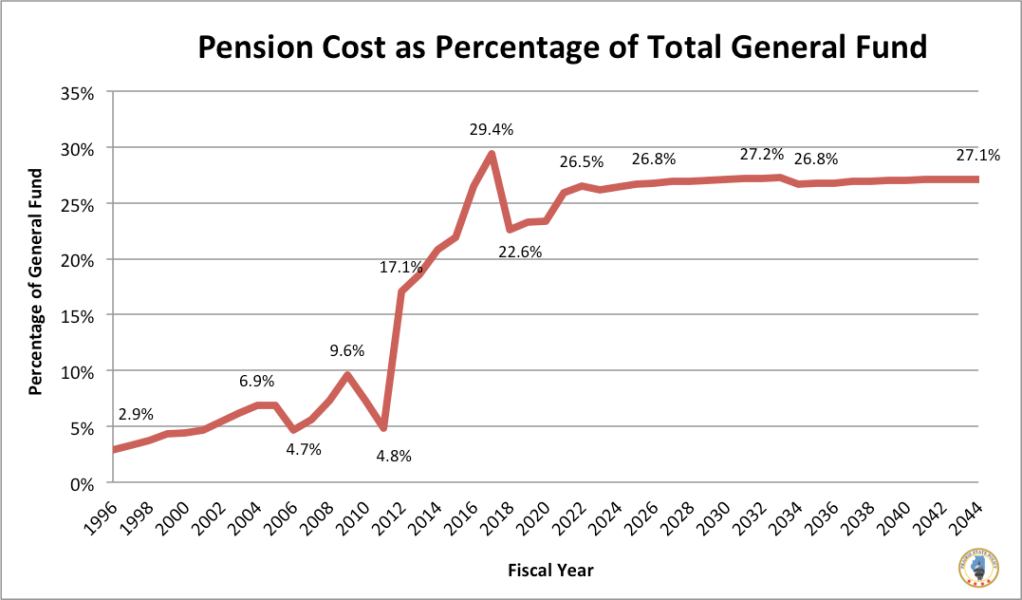

In 1994, then first term governor Jim Edgar signed legislation that hoped to stabilize the state’s retirement systems through mandatory, gradually escalating investments. The state was coming out of a recession, and there was pressure to ease fiscal burdens by adjusting the payment schedule based on current economic conditions. According to Crain’s Chicago Business, Governor Edgar set a goal of having the systems 90 percent funded by 2045. However, his administration altered the payment schedule so that payments for the first fifteen years were set artificially low – freeing up funds for the state to make short-term investments – then ramped up in the long-term. As years went on, the state’s mandatory payments heavily increased year by year. Figure 1 below illustrates this phenomenon.

While the Edgar ramp took pressure off the budget in the short-term, skipped payments proved to be detrimental in the long run. In 1996, pension contributions made up only 2.9 percent of the state’s total general funds. By 2015, this increased to roughly 23 percent, imposing a drastic fiscal burden on the budget to invest in key public services and goods, such as education.

A 2013 report by the Illinois Commission of Government Forecasting and Accountability (CGFA) estimated the ramp added $1.3 billion in liabilities. This has led the U.S. Securities and Exchange Commission to charge the state for misleading pension disclosures. According to the S.E.C, “The statutory plan structurally underfunded the state’s pension obligations and backloaded the majority of pension contributions far into the future. This structure imposed significant stress on the pension systems and the state’s ability to meet its competing obligations – a condition that worsened over time.” Our next piece will look at decisions made in the 2000s that contributed to the rising underfunded pension liabilities.

Discover more from Prairie State Policy

Subscribe to get the latest posts sent to your email.

One thought on “Dissecting Illinois’ Pension Problem Part IV: History of Neglect (The 1990s)”