What are Pensions?

Pensions are money owed to former public employees as severance to their public service and work. Recipients of these benefits in Illinois include teachers, police, firefighters, state employees, judges, and more. Recipients start collecting this benefit at retirement.

How Pensions Work

Both the pension recipient and Illinois taxpayers pay into a specific pension fund. For the recipient, the amount diverted to the pension fund is a set percentage of their salary and this continues to be made over the course of employment. Once the employee retires, they are owed a certain amount of money each month as retirement income. Pensions are often sometimes referred to as a type of annuity for the public sector.

Perhaps the most important component to understanding pensions is understanding the relationship between how much revenue is being contributed to the fund and how much is being paid out. Simply put, analyzing those who are making contributions (employee and taxpayer contributions) to the fund and those who are retiring and drawing the benefits is paramount to understanding the solvency of pension funds. If you have more people retiring and collecting the benefits at a greater rate than revenue being collected to sufficiently fund the system, there is a definite concern for solvency moving forward.

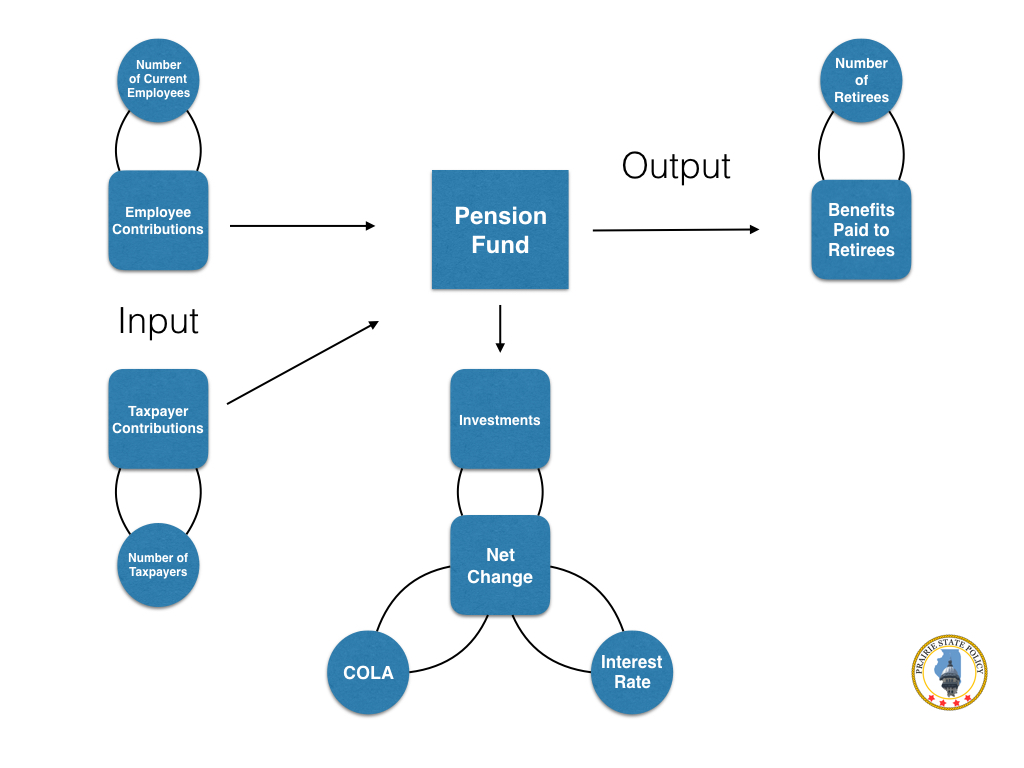

Figure 1 below illustrates this phenomenon. While there are more details that affect the system, the model below is intended to serve as a basic example.

Some notes with the model above:

- The non-arrows represent dependence among variables. This is necessary to include in the model because it stresses the relationship between the amount of revenue coming in to fund the pension and the amount of money that is outputted to pay the retirees. For example, while employee contributions are a main component that fuels pension funds, the number of employees that are making contributions to the fund is just as necessary.

- Overtime, more and more employees will reach the age of retirement. This will cause the amount of payout of benefits to fluctuate overtime as well as the amount of people eligible to start receiving the benefits. Consequently, we would also except retires receiving benefits to die as they age or their beneficiary. In effect, the amount of retirees and the amount in benefits the state would need to pay to these recipients will fluctuate overtime.

- Investments: Once revenue is collected, it is invested so that money can keep pace (or exceed) inflation and benefits can be sufficiently paid overtime. How the investments perform are generally dependent upon two main variables:

- Net Change: The calculation of how much pension funds are estimated to change based on two main variables, COLA and the Interest rate.

- COLA: This stands for “Cost-of-Living Adjustment,” which is an increase the benefit will grow each year for the recipient in order to keep pace with inflation. When the increase is a “fixed amount,” this is referred to as a defined benefit. When the benefit is dependent upon market variables, this is known as a defined contribution.

- Interest Rate: Because the performance of some plans are dependent upon how the market is performs, the interest rate is a important factor in both how much the recipient will receive and how much the public entity needs to pay out. Poor market performance will result in adding more underfunded liabilities as the amount that the fund is making is not sufficient with the amount needed to be paid to recipients.

- Net Change: The calculation of how much pension funds are estimated to change based on two main variables, COLA and the Interest rate.

- Employee contributions (annual): This is dependent upon the number of active employees contributing to the fund. This flow results in less debt (e.g., as employees contribute, they “remove debt”).

- Benefits Paid to Retirees (annual). The amount the state pays out per year to retirees or their beneficiary. This is dependent on the number of retirees that are owed benefits. The greater the amount, the more money the state needs.

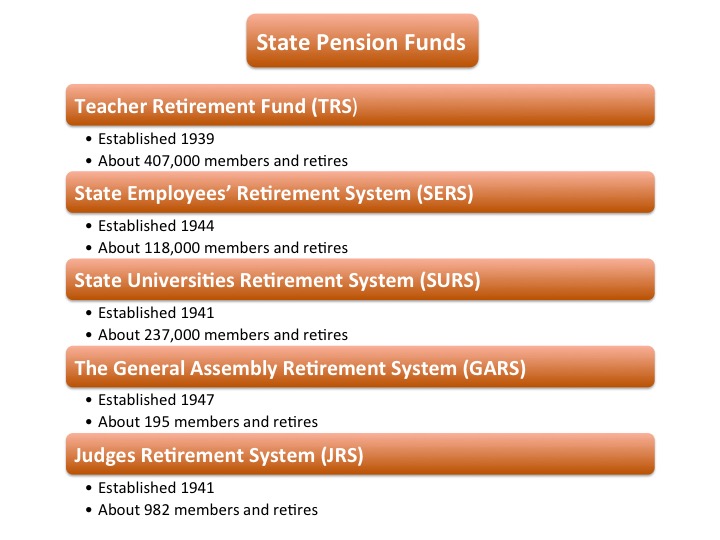

Illinois’ Pension Structure

There are a total of 667 pension funds for public employees in Illinois. However, all but five of these are employees who work for municipalities or the county. There are five main state pension funds. Figure 2 below illustrates these funds:

The State of Illinois collectively pays out about $9.5 billion to recipients of just these five pension funds per year. The next piece, Part III, will look into certain categories that recipients may fall into, Tier I and Tier II employees.

Discover more from Prairie State Policy

Subscribe to get the latest posts sent to your email.

One thought on “Dissecting Illinois’ Public Pension Problem Part II: Modeling Pensions”